After struggling to understand the economic

survey and budget documents for more than 36hours, I have concluded that at

least in matters of government, ignorance is actually bliss.

In my view, a presentation that makes

overwhelming use of technical jargon, complicated arguments, and statistical

manipulation, usually implies lack of conviction in the presenter. Moreover, a

presentation which does not take into consideration the comprehension level

and linguistic abilities of its audience is a futile exercise. Usually such

presentations are the outcome of either poor communication skills of the presenter;

or mala fide intent of the presenter. Presenters tactically overuse technical

jargon and complicated arguments to overwhelm the audience so that they could

be distracted from noticing the shortcomings.

In my view, the latest budget and economic

survey are clear cases of poor communication. They follow the principle of “Form

over Substance”, as these conceal more than what they reveal. I would not go to

the extent of terming it a case of mala fide intent, but there is

definitely incongruence and lack of conviction on many counts.

In her speech, the finance minister used a lot of

jargon like “digital economy”, “Fintech”,

“Technology enabled development”, “energy transition”, “Unified Logistics

Interface Platform”, “Chemical-free Natural Farming” “G2C, B2C and B2B services”,

“Drone as a service (DaaS), “Battery as a Service (BaaS), “Design Linked

Manufacturing (DLM)”, “Blockchain”, “Digital Banking Units”, “Deep-Tech”, etc.,

The audience for her budget speech is supposed to be the members of parliament

and 140crore Indians. I am sure a large majority of this audience (including many

of her cabinet colleagues) does not understand this jargon. Obviously, the

economic survey and budget presentation has been prepared by “professional

type” managers engaged by the government, who may be totally disconnected from

the ground realities.

There are some glaring

examples of goal incongruence in the budget. For example, climate change,

energy transition, clean energy etc. have been cited as core tenets of new

development paradigm. However, using ethanol produced from sugarcane, running

electric vehicles on batteries charged with thermal power, and burning biomass

pellets with coal in thermal plants do not concur with this tenet. It is widely

acknowledged that sugarcane is one of the most water intensive crops.

Admittedly, water in India is highly energy intensive. Ethanol extracted from

sugarcane produced using water pumped through diesel pump sets is not exactly

clean fuel and it certainly does not help in climate change efforts.

The finance minister said

that “five to seven per cent biomass pellets will be co-fired in thermal power

plants resulting in CO2 savings of 38 MMT annually.” The research however shows

that biomass burning in power plants emits 150% the CO2

of coal, and 300 – 400% the CO2 of natural gas, per unit energy produced. (see

here)

The finance minister

stated that “The animation, visual effects, gaming, and comic (AVGC) sector

offers immense potential to employ youth”. Only a few years ago the government

had banned some AVGC Apps arguing that these are misleading the youth of the

country. Many organs of the government and the Political party of FM vehemently

argue that social media is distracting the youth of the country from the right

path. How does she reconcile these two? If there is recognition within the

government that social media is now integral to the economy, then the first step should

have been to lift the ban from TikTok.

This is Tuesday afternoon

and Children of the household are uncertain about getting the evening meal. The

finance minister is asking the children to make merry because she will be

hosting a gala dinner on Sunday.

Millions of Indian youth

who are looking for employment cannot wait through the Amrutkaal to get jobs.

They needed it yesterday. The government managers need to understand that if an

engineering graduate does not get a job within 6months of his passing out, the

chances of his getting a suitable job for the rest of his life reduce materially,

because he has to then compete with the fresher graduates.

The finance minister

emphasised that “Our government constantly strives to provide the necessary

ecosystem for the middle classes – a vast and wide section which is populated

across various middle-income brackets – to make use of the opportunities they

so desire.” A plain reading of this phrase would mean the government has done

enough for the middle classes. Now they are on their own.

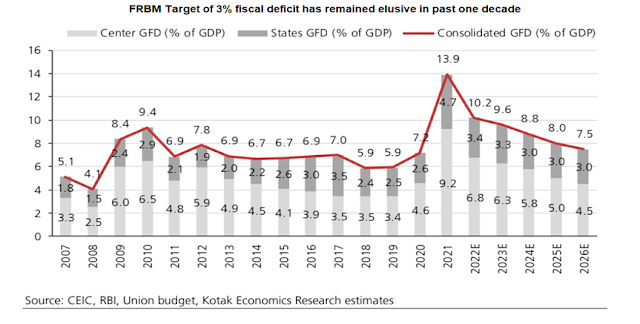

RBI and most experts have

cautioned the government that the recovery from pandemic lows is fragile and

would need to be kept supported. Disregarding the advice, the government has

decided to fully withdraw most Covid related stimulus. Food and Fertilizer

subsidies have drastically cut. Rural development and social sector allocations

have also been cut. Expenditure on health has also been cut. Of course, this

all is done in the name of fiscal consolidation. I understand it is a tough

choice , but if I must choose between 1000 km of new highway and food to

800million people for one year, I will choose the latter.

The finance minister

defined “transparency of financial statement and fiscal position” as a fundamental tenet of the budget process. However, it appears that in some cases the

economic survey and budget documents have tried to evade or manipulate the

statistics. The data points have deliberately chosen to show the latest numbers

in good light. Points that could have hurt stock markets were evaded or manipulated

in the budget speech. In some cases numbers have been stated ambiguously.

For example consider the

following:

·

The

finance minister skipped mentioning about restricting the practice of bonus

stripping.

·

The actual

growth in capital expenditure is yet to be figured out by experts.

·

The

government has proposed Rs2/litre excise duty on diesel wef October 2022, i.e.,

2HFY23. Instead of saying it in these many words, the FM chose to say “Blending

of fuel is a priority of this Government.

To encourage the efforts for blending of fuel, unblended fuel shall

attract an additional differential excise duty of ` 2/ litre from the 1st

day of October 2022”. As per her government order, it is mandatory to blend

ethanol with petrol. Only high speed diesel is unblended fuel.

·

In last

year's budget a whole deal of emphasis was given on disinvestment and

privatization of banks etc. Nothing happened in the current year. The finance

minister evaded even a cursory mention of this in her latest speech. If the

government is so concerned about markets and investors, does it not hold any

accountability to investors who would have acted on the promise of

disinvestment and privatization?

·

The

finance bill makes a significant effort to tighten the regulation over

charitable institutions. There was no mention of this in the budget speech.

There is so much more to say, but I think I

have broadly made my point.