No margin for error – a few more thoughts

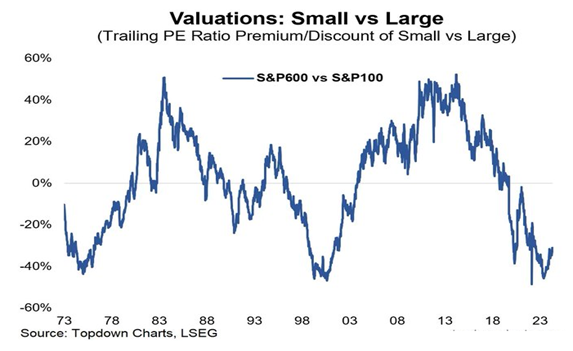

Yesterday’s post ( No margin for error ) evoked a multitude of thoughts. Some readers have challenged the premise that the broader markets, especially the small-cap stocks, have sharply outperformed the large-cap components of the benchmark indices. They have argued that — · Nifty Next 50 Index (YTD higher by ~21%), which comprises the top 50 stocks outside the Nifty50 (YTD higher by ~2.7%) universe, has performed much better than the Nifty Midcap100 (YTD higher by ~9%) and Nifty Smallcap 100 (YTD higher by ~10%) indices. · If we exclude private banks and IT services stocks from the Nifty50 universe, the rest of it has performed better than the broader market indices. · These statistics (index performance) completely fail to present a correct picture of the market. The narrative that small caps have done better than large caps is mostly...